Nvidia Thesis Change

Nvidia Q1 FY2027 Earnings

Nvidia (NVDA) Q1 FY27 results were well above guidance and consensus as expected. The Nvidia supply chain is closely monitored and even the multi-billion dollar beat-and-raise are not a mystery and in line with buy-side expectations. In a sense, Nvidia retail earnings option plays mostly bomb due to this dynamic. To drive the stock, management needs to deliver something beyond just a beat-and-raise. Did we get that in the Q1 earnings call? We discuss that later in the article.

Results And Guidance Continue To be Exceptional

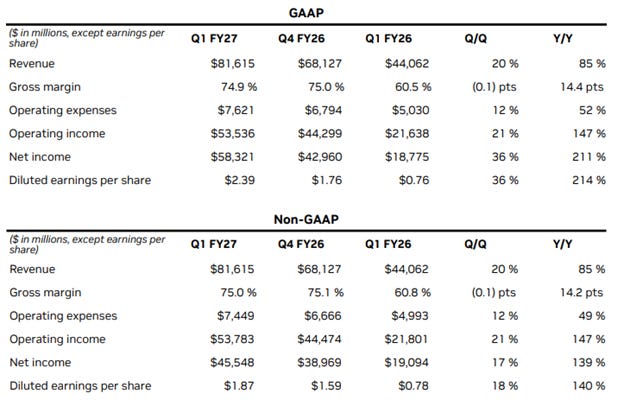

There should be little doubt that the numbers, driven by demand that went parabolic due to agentic AI, are exceptional. Q1 revenues of $81.6B exceeded yesterday’s leader Intel (INTC) peak yearly revenue of $79B from 2021! The Q2 revenue guidance of $91.0B at 75% margin is even more spectacular.

Nvidia continues to go further into territory never seen before (image below).

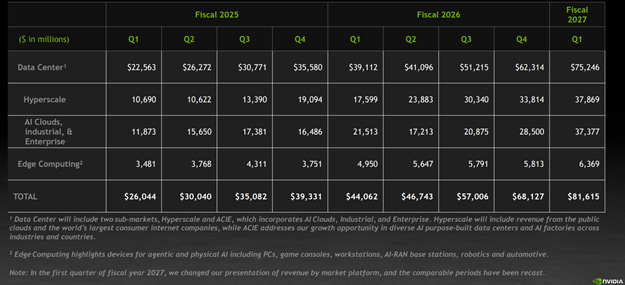

In an interesting move, Nvidia changed its reporting structure starting Q1 (image below). There is strategic significance to these splits and will be addressed later in the article.

With the change, gone are disclosures about Gaming, ProViz, Auto and OEM/Other segments. Instead, Nvidia now consolidates all non-data center businesses into “Edge Computing” bucket. This is a welcome change as the older splits have become largely irrelevant considering the sheer size of the data center business. Even the consolidated Edge Computing segment is too small to matter but could become meaningful in the course of time.

The Company also split the data center segment into two subsegments – Hyperscale and ACIE. Hyperscale will include revenue from the public clouds and the world’s largest consumer internet companies and ACIE groups diverse AI purpose-built data centers (neoclouds, etc), and AI factories across industries and countries.

The exceptional data center growth was driven more by networking than computing. Computing revenue of $60B was up 77% year-over-year and networking revenue of $15B nearly tripled year-over-year. While networking demand leads GPU somewhat, the magnitude of difference suggests that the growth is likely from market share expansion. The large networking growth is likely indicative of Nvidia gaining share at the expense of Broadcom (AVGO).

On a year-to-year basis, Hyperscale grew faster than ACIE (image below). This is likely being driven by the hyperscale customers putting the pedal to the metal on capex.

On the balance sheet front, the most notable development is that, as of April 26, 2026, Supply Related Commitments jumped to $119B from $95B in the previous quarter. Of these, $95B will be paid in the remainder of fiscal year 2027 and the remaining balance will be paid in fiscal years 2028 through 2031. This is suggestive of Nvidia’s most favored nation memory pricing expiring no later than the end of FY2027. In other words, Nvidia is unlikely to have significant cost edge on memory compared to peers beyond FY27. By the time Rubin is in volume production, it will likely have no meaningful memory cost advantage against AMD MI400.