Micron Blasts Past Expectations

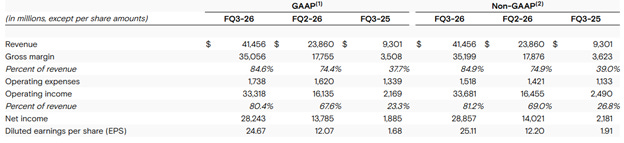

Micron (MU) delivered stunning Q3 FY26 results somewhat reminiscent of the type of growth we have only witnessed once before – Nvidia (NVDA) blowouts in the early part of AI ramp. All Q3 numbers were well ahead of expectations (image below).

But what is even more stunning was the guidance – especially the 86% gross margin guidance. Although this is in line with Beyond The Hype expectations, it is well ahead of market expectations.

For gross margins to go from 84.6% in FQ3 to 86% in FQ3, ASPs need to increase by about 10% - in a single quarter. Where will most of the ASP growth come from?

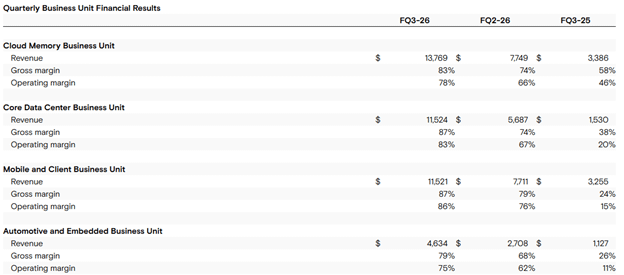

Look at the table below.

Note that the Cloud Memory Business Unit margins are lagging compared to the two other business units. That is because this group consists of HBM products which once were the highest margin products. Savvy customers like Nvidia secured HBM capacity and pricing last year before the meteoric rise in memory pricing. Those commitments will dwindle away as time passes on. Beyond The Hype expects that most of the ASP increases in the coming quarters will come from this business unit. As a result, GPUs and accelerators are going to see big price increases in the coming quarters.

With memory demand continuing to increase and with many customers still not having secured long-term agreements, the memory prices, as high as they are now, will continue to go up. While the SCAs will limit the price increases somewhat, HBM price increases will contribute handily. Expect Micron’s margins to continue to climb for at least a couple more quarters.

Earnings Call Highlights

The biggest highlight of the earnings call was the announcement of Company’s Strategic Customer Agreements which run from CY2026 through CY2030. There were also other key comments about demand and sustainability that Beyond The Hype believes are sentiment changers for investors and analysts. The following is a summary of the highlights:

“Even as we expect industry supply to improve gradually in 2028, we currently do not have line of sight as to when memory supply will be able to catch up with increasing demand. “

“We are pleased to announce that we have completed 16 SCAs with customers across the data center, consumer, and auto market segments. These SCAs accelerate the transformation of our business model, enhance partnership in technology and innovation, and provide customers with contracted supply assurance. Typically, these agreements have a five-year term from calendar 2026 through the end of calendar 2030. Automotive agreements generally have a three-year term. The 16 signed agreements represent roughly 20% of our DRAM volume and a third of our NAND volume over this period. These SCAs include four very large customers and three medium-sized customers. The remaining agreements relate to smaller customers from the automotive industry and represent our commitment to the important sector. When completed, we expect approximately half or more of our company revenue to be under these SCAs with customers across end markets.

Our customer value, our U.S. supply plans, this is reflected in our SCAs. These SCAs are structured as take or pay agreements with binding commitments to purchase specific volumes over this multi-year term. The largest agreements generally have a ceiling price for existing products at the current CQ2 market price and a floor price through the term of this agreement. Several SCAs, which account for a modest portion of the SCA related revenue, include either fixed prices or have no price bands associated with them, where pricing will be subject to market conditions. When all planned SCAs are executed, agreements with either fixed prices or price ceilings at or close to current CQ2 market prices are expected to be approximately 40% of our revenue. For SCAs which do contain such price bands, pricing is designed to stay within this floor to ceiling level through the course of the term.

This pricing visibility will help our SCA customers across market segments to better manage their business and grow their demand. For our SCAs with price bands, the floor price enables a very robust gross margin for Micron, well above our peak quarterly margins in any past cycle.”

“Humanoid robots carry 10 times the amount of memory as an average L2+ vehicle, and we expect a sustained, substantial, multi-decade memory demand cycle to begin in the latter part of this decade.”

“So with respect to HBM, first of all, very, very pleased with our HBM4 product and Micron’s shipments already of HBM4 of over $1 billion. HBM market share, we strategically are choosing it to be close to our DRAM share. And this is important because of the trade ratio of HBM. It consumes, as you know, a significant amount of wafers and puts pressure on non-HBM supply in the industry. So targeting our HBM share close to our DRAM share strategically enables us to supply our diversified end markets, customers across all end markets, data center, consumer, automotive, industrial, the markets that need non-HBM supply.”

“So Krish, we’re not going to get into specific pricing discussions, but I just want to note again, that I said, that the gross margins at the floor will be well beyond the peaks that we experienced…”

“We see 2027 overall tight. We have said we see tightness continuing beyond 2027, working hard to bring up supply, but we have shared with you that it takes a long time to bring up the additional capacity that is needed to support the customer demand, the additional wafer capacity. And of course, technology transitions and the less bit gain that they give per node as well as the HBM trade ratio put tremendous pressure on the overall supply growth as well. So supply -- even in 2028, when supply begins to improve gradually, we see that the demand will continue to be on a robust trajectory as well because these AI trends are very long-term trends. AI is still in very, very early innings.”

Prognosis

The results and the management commentary change Beyond The Hype current thesis about Micron in three important ways:

Keep reading with a 7-day free trial

Subscribe to Beyond The Hype - Looking Past Management & Wall Street Hype to keep reading this post and get 7 days of free access to the full post archives.