Intel Commentary Continues To Not Show Any Signs Of Revival

Intel (INTC) with its Q1 earnings commentary once again did the dance of beating previous quarter guide but lowering current quarter expectations. Not surprisingly, the market could see through the charade and the stock went down nearly 10% post-earnings.

Intel cited 40M AI PC shipments in 2024 as a strength but it is unclear how this AI PC ramp will be helping Intel. Technically, AI PC strength should manifest as a slight ASP uplift or as increased units driven by PC refresh but there is no evidence of benefit from either. Whether this indicates weakness in other parts of the CPU business is something that time will tell.

Intel cited Meteor Lake demand as being stronger than previously expected but once again there is no evidence of that in the guidance. While Intel cited Meteor Lake supply issue as a problem, it is unclear if this was due to packaging issues that management cited or poor fab yields. Given the rushed process ramps, the chance of a poor fab yield is high. Intel noted that Meteor Lake supply situation gets better over the coming quarters and Lunar Lake and Arrow Lake will add to the H2 strength. it was unclear if Meteor Lake supply challenges impacted Q1 or management cited it only in the context of Q2 guidance. Whatever the Meteor Lake ramp mechanics, it is safe to say that there is not going to be much of a recovery at Intel until the Company can guide up instead of guiding down.

If one were to take Intel commentary at face value, the read thru is positive for Advanced Micro Devices (AMD). The stronger than expected PC demand and Meteor Lake supply challenges should mean that AMD would have gained more share than usual at the high end of the PC market.

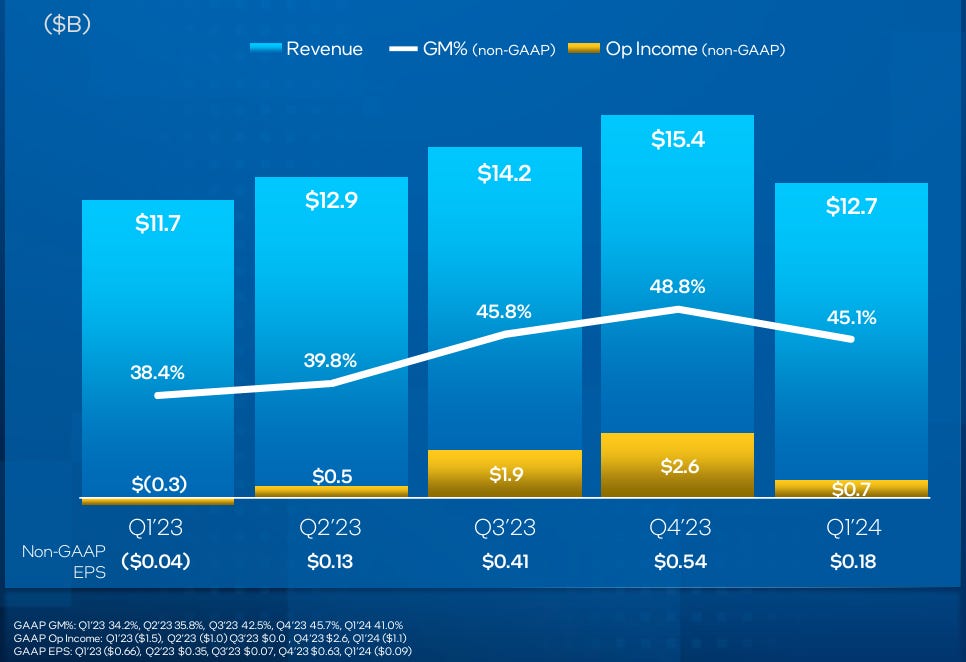

On the plus aide, Intel has been driving down its cost structure and we can see a billion dollar improvement in operating income from Q1 2023 level on a billion dollar growth in revenues. Although Intel’s costs are not reducing at a pace they should, they are declining.

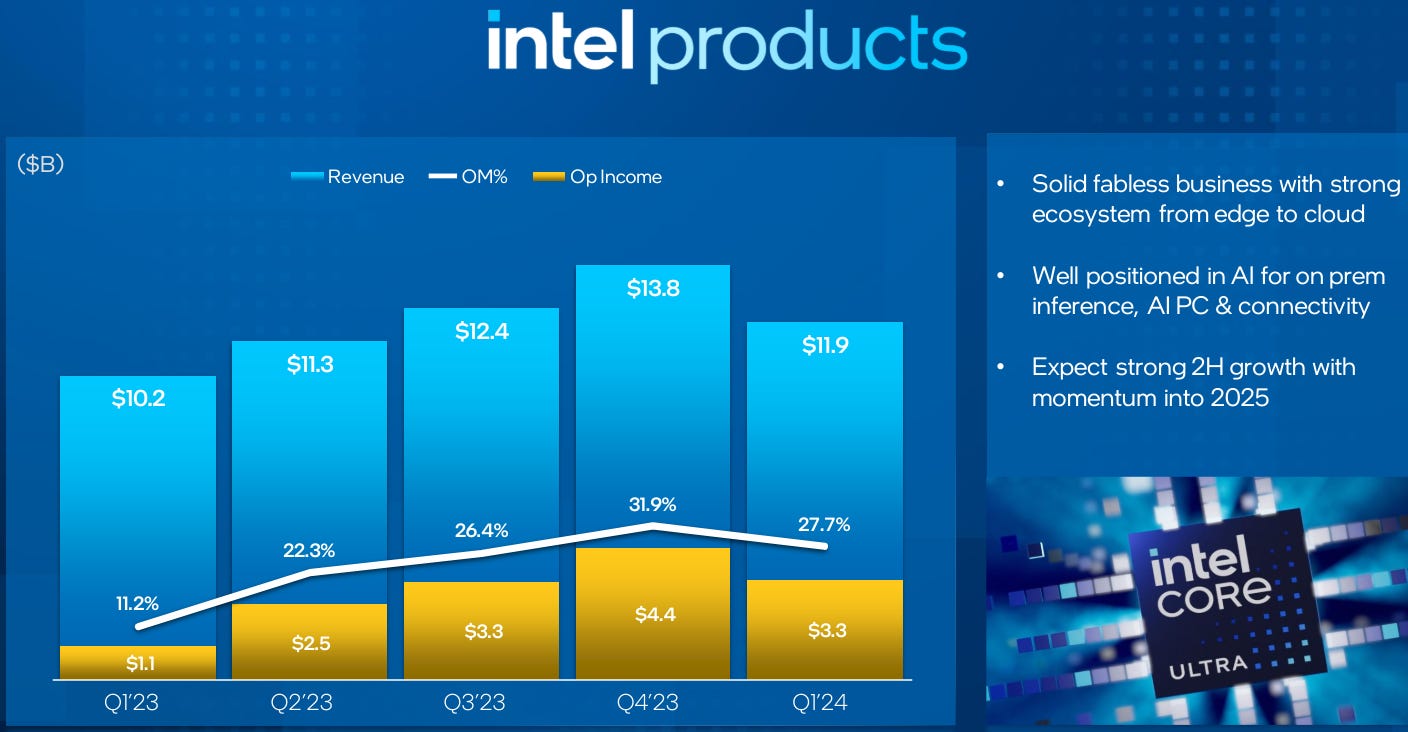

The newly constituted Intel Products division shows an even stronger picture. Operating income grew $2.2B on a $1.7B revenue growth (image below).