Intel Capacity Crunch Is A Big Problem

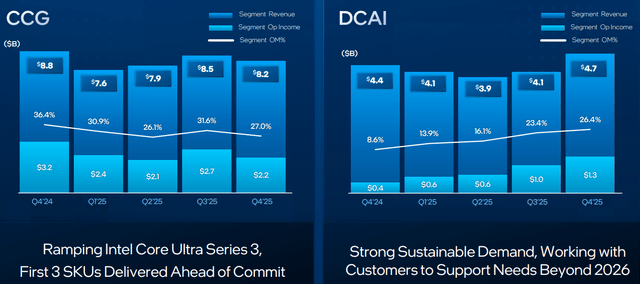

Intel (INTC) delivered a strong Q4 beating on revenues, margins, and EPS as expected. The top line, as can be seen from the image below, was flat with Q3 and below Q4 2024, but was ahead of expectations as Intel divested assets (Altera) and cut some non-strategic operations. Management noted that if not for the guided supply constraints, the results would have been stronger.

CCG revenues were down in a seasonally strong quarter but once again this was expected as Intel diverted capacity from CCG to DCAI. The unquestionable highlight of Q4 was the strong uptick in DCAI revenues – both on a sequential and year to year basis. (image below)

Another highlight was that Intel saw strong growth in the Networking ASIC business. BTH’s understanding is that this business is likely from Google (GOOG) networking custom silicon. Intel was able to do a last minute save on the business that was about to go to AMD.

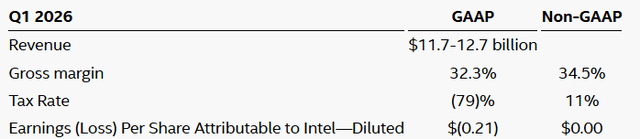

Management said several times during the call that DC AI demand was very strong. The demand narrative came into clash with the massively disappointing guidance which had sequential drop in revenues and gross margins (image below)

For Q1, the Company forecasted a more pronounced revenue decline in CCG than in DCAI as Intel continues to prioritize internal supply to server end markets. But why would revenues decline in a world where the agentic and data center demand is off-the-charts?

It turns out that the answer has multiple components:

The Company has been shipping from finished goods inventory to post the strong (relatively speaking) Q3 and Q4 numbers. Now that the Company has chewed through the inventory, the supply situation is more hand-to-mouth. In other words, Intel’s Q1 capacity is closer to Q1 guidance! This is a shocking disclosure and should cause analysts to take down Intel number for the year.

Intel is sitting on nearly $12B of inventory but it is mismatched to Company’s needs. This shows a rapid change in the nature of demand but also shows poor read of customers.

And, finally, the implication of Intel’s commentary was that its yields for 7nm and 3nm are also poor (and not just Intel 18) which lowers possible capacity. Simultaneously, it is clear that Intel is not getting as much capacity as it would like from TSMC (TSM)

Management noted that Q1 would seasonally strong if not for the capacity challenges. Things are not pretty on the capacity front: