Competitive Risk Starting To Materialize At Broadcom

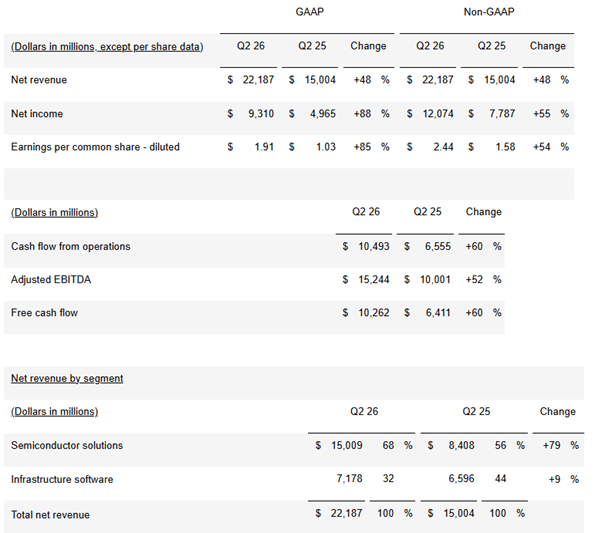

Broadcom’s Q2FY 2026 earnings largely came above expectations although the AI specific numbers were on the softer side of expectations. The revenue and income line items continue to indicate ongoing strength (image below).

Q3 FY2026 guidance was also strong (image below) although the gross margin deterioration shared during the call, due to increasing AI semiconductor mix, was not to investor liking.

However, neither the margin concern nor the slightly softer AI numbers were the reason the stock plummeted. This article summarizes the highlights of the call and the likely reasons why the stock reaction was adverse.

Highlights

- AI semiconductor business continues to be very strong. For FY2026, the Company expects AI semiconductor revenue of $56B, up approximately 180% from FY2025.

- Networking continued to put up a strong show and represented almost 40% of Q2 AI revenue.

- During the quarter, bookings for AI semiconductors were over $30B – about 3X the $10.8B the Company shipped in Q2.

- Broadcom mentioned it delivered accelerator silicon to OpenAI and said it is on track for production in late 2026. Management noted that it has a contractual commitment to deploy 1.3GW in 2027 as part of the larger 10GW deployment by 2029. While management did not specify when the silicon was delivered, even assuming a mid Q2 delivery, the schedule seems aggressive.

- For Meta, management noted that the initial order for 1GW, which includes XPU and networking, has been received and will start delivery in H2 2027. Broadcom expects to deploy total 3GW through the end of 2028.

- For the other two customers, Broadcom expects shipments to begin late 2026 and accelerate into 2027. To date, the Company has received purchase orders totaling $6B. Note that while this is respectable, it is far smaller opportunity than the others mentioned by name.

- The Company guided 10GW in back-half loaded shipments in 2027 and that did not change. The Company expects a lot more GW in 2028. Management noted that three months back the visibility was into 2027 but now into 2028.

- Management reiterated FY27 AI semiconductor revenue guidance to be more than $100B mainly on the strength of Google (GOOG) (GOOGL) orders. While strong, this represents no change from previous guidance when the market was expecting an upward revision based on Google AI strength. This was likely one of the bigger reasons for the stock weakness.